Texas Health Insurance Introduction

It's complicated!

Let's go through the top-level view of how to really get the most value knowing that you can reach out to us with any questions for free assistance!

First...our credentials:

This is what we'll cover:

- Why even get Texas health insurance

- The big 3 Texas health markets

- The individual family market including the Exchange

- The Texas Medicare market including Advantage, Supplements, and Part D

- The Texas small business health plan market

- Get Free Assistance across all three markets

Let's get started. Here, we�ll give a general overview but point you to the best pages for the topic.

Why even get Texas health insurance

We've covered this partially with the Medicare market, but the same applies across the board.

People will say... "I'm healthy. I don't even go to the doctor."

The issue today is around hospital costs and accidents, injuries, and the recent explosion in clotting or cancer issues only make this worse.

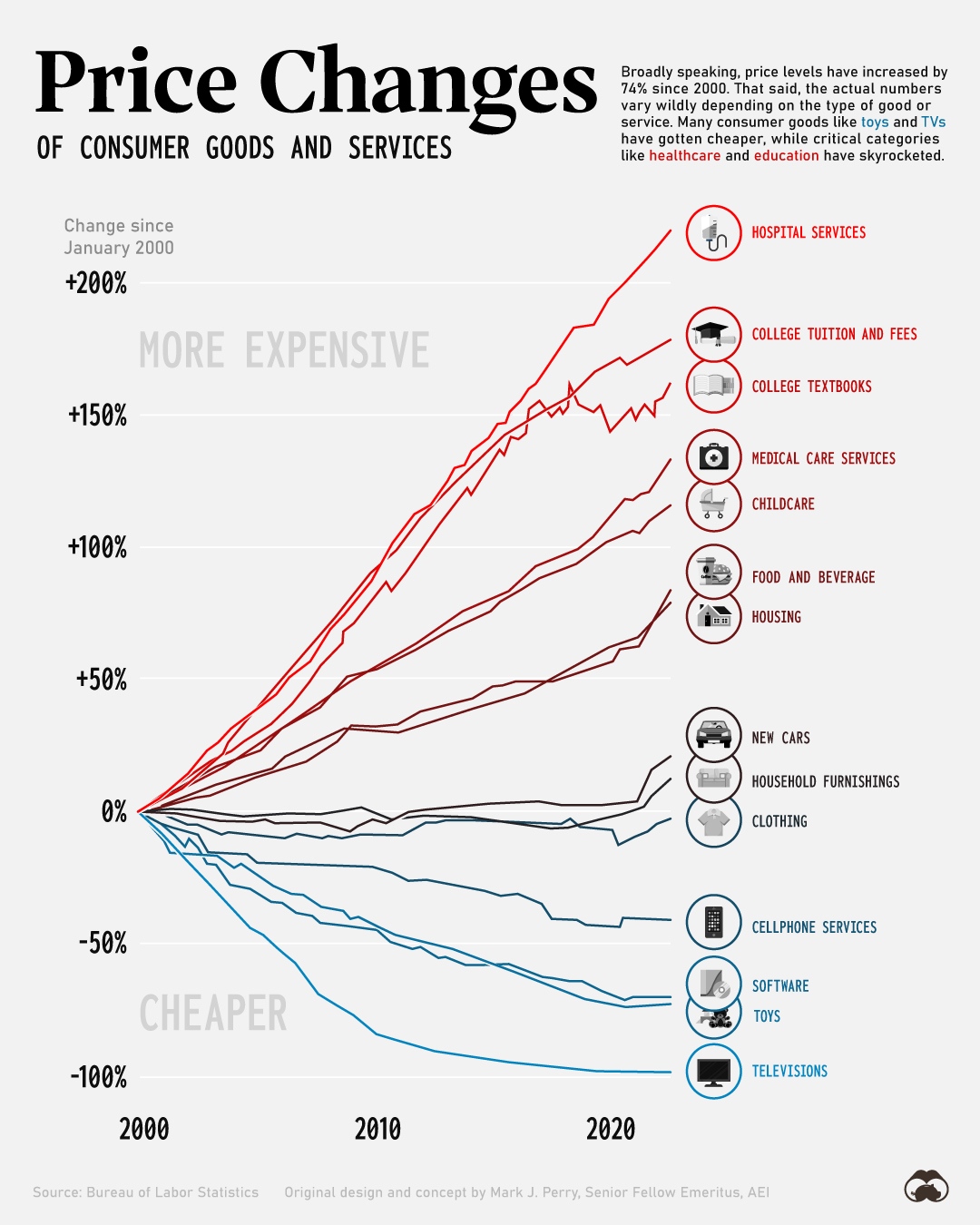

Look at the trajectory:

We see medical costs of $500,000+ routinely and one of our clients recounted his story:

"$250K for each hour his heart was offline during open heart surgery (sudden heart attack). Total... $5 million!"

This isn't to scare anyone. It's to explain the risk of not having coverage in Texas, especially when we might be able to find major medical plans for very low costs.

There are now subsidies based on income that can reduce premiums all the way down to zero in some cases.

Run the quote below and enter your best estimate for income (AGI on the 1040 tax form). It's not worth the risk that can wipe you out for years to come.

Let's turn our attention to how the Texas health market is divided. Very different markets!

The big 3 Texas health markets

There are three main markets in Texas:

- Individuals and Families

- Medicare-eligible people (usually age 65 or older or younger people on disability)

- Business health plans: Small Business is now 1-100 employees; Large Business 100+

Completely different markets!!

Let's hit the highlights and point to key articles to guide you.

The individual family market including the Exchange

This is for people under age 65 who don't get coverage through an employer.

- Almost all enrollment is now through the Texas Exchange

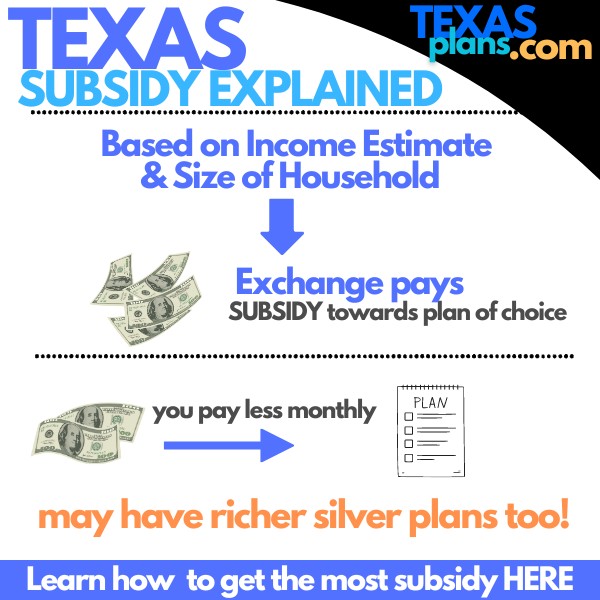

- Benefits, rates, and networks are identical on or off exchange

- Rich subsidies (reduce monthly premium) and richer silver benefits based on income

It's really about subsidies these days. We see premiums down to zero dollars these days.

Some key guides:

- How to compare Texas exchange plans

- Getting the most subsidy

- How to compare the Texas exchange networks

Reach out to us with any questions!

Zero cost for our assistance:

Call 800-320-6269

help@texasplans.com

Chat online here

Pick a time to talk here

The Texas Medicare market including Advantage, Supplements, and Part D

This gets a little more complicated (of course!).

There are three main "markets" for people eligible for Medicare:

- Medicare Advantage plan - mostly HMOs that wrap around traditional Medicare

- Medicare supplements (Medigap) - work like PPOs with more flexibility

- Part D - Medication plans that usually work alongside Medigap plans

You can quote all three here:

There's lots to cover here, but a few key guides:

Medicare really gets more complicated, so reach out to us with specific questions!

Zero cost for our assistance:

Call 800-320-6269

help@texasplans.com

Chat online here

Pick a time to talk here

The Texas small business health plan market

Completely different market with a whole set of new rules!

This is for companies that want to offer employee benefits to attract and keep staff in more competitive industries!

It may also be for small businesses that want access to the full PPO networks that are no longer available on the individual family market, and we look at how this works in detail at the link.

A few notes:

- There's a line between Small and Large business at the 100 employee level

- There may be penalties for not offering health coverage to employees with 50+ full-time equivalents (reach out to us on this piece)

- We can cap the employer's exposure and give employees flexibility to pick the plan that works for them

We're happy to run these numbers across the board and see who's priced best for your situation.

We generally use this strategy and then craft it around the employer's cost requirements.

You can request your quote here:

Of course, reach out to us. Happy to help!

Texas health agents with 5 Star Google reviews

Finally, don't go it alone.

We've helped 10's of thousands of people find the best options across all three markets for years!

There's zero cost for our assistance and if you look at the reviews, we really do try to help people.

Zero cost for our assistance:

Call 800-320-6269

help@texasplans.com

Chat online here

Pick a time to talk here